Emergency Fund Examples for Renters, Homeowners and Families

Reviewed 19 May 2026. Uses UK emergency-savings guidance and practical household examples. Treat the figures as planning cases, not national averages.

“Three to six months of expenses” is a useful rule of thumb, but it is too vague on its own. A renter with low fixed costs, a homeowner with an old boiler and a family with one main earner are not carrying the same risk.

Three to six months of essential outgoings is a useful rule of thumb. The right number depends on job security, dependants, housing situation, health, transport needs and how quickly you could cut spending if income stopped.

Example targets by household type

The examples below are not national averages. They are planning cases. The point is to show how the same rule changes once housing, dependants, transport and job security enter the picture.

| Household type | Example essential monthly costs | Starter buffer | 3 months | 6 months | When to lean higher |

|---|---|---|---|---|---|

| Single renter | £1,600 | £1,000 | £4,800 | £9,600 | Variable income, car dependence, no family support |

| Homeowner couple | £2,200 | £1,500 | £6,600 | £13,200 | Mortgage, older property, one main earner |

| Family with children | £3,500 | £2,000 | £10,500 | £21,000 | Childcare, two cars, self-employed income |

First build a small starter buffer. Then aim for one month of essentials. Then three months. Six months is useful, but it does not have to happen before every other financial goal.

Renters vs homeowners

Renters may need flexibility for moving costs, deposits or a sudden job change. Homeowners may need a larger buffer because repairs can be expensive and urgent. A broken boiler, roof issue or insurance excess can quickly turn a small emergency fund into no emergency fund.

Families usually need more margin

Children make the buffer less optional. Childcare, school costs, food and transport are not easy to pause. If the household relies heavily on one income, a longer runway can be worth the slower progress elsewhere.

Where to keep the money

An emergency fund is not supposed to be an exciting investment. It should be accessible, stable and boring. Easy-access savings accounts and cash ISAs can both make sense depending on your tax position and ISA plans. FSCS protection for eligible deposits rose to £120,000 from 1 December 2025, per eligible person, per UK-authorised firm.

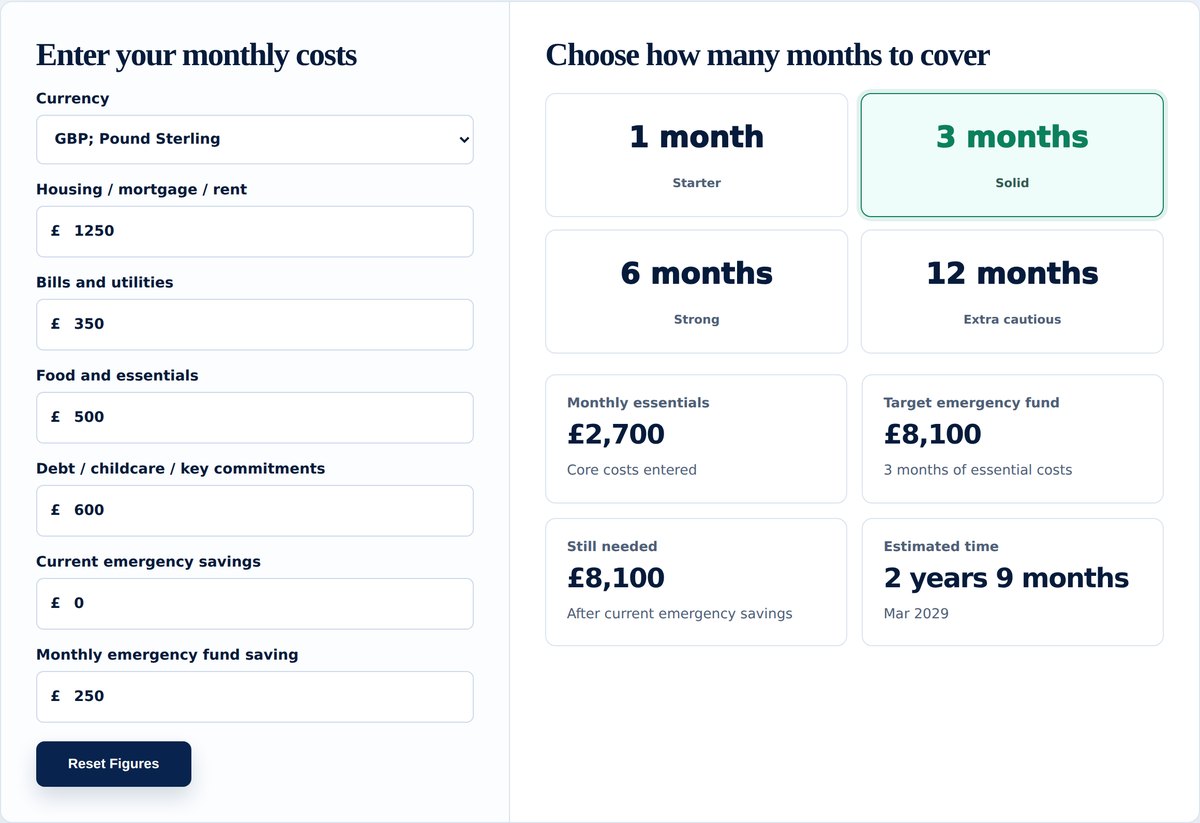

Use the calculator

Use the Emergency Fund Calculator to set your own target and time it against your monthly savings rate. Once your fund is in place, the Investment Calculator can help model longer-term investing.

Sources and useful reading

This article is for general information only. It is not financial advice or a personal recommendation. The examples are here to help you think through your own emergency fund, but they cannot tell you what is right for your circumstances.

Emergency money is usually held in cash because access and stability matter. Interest rates, inflation and tax rules can still change over time. If you choose to invest money instead, remember that investing involves risk and the value of investments can go down as well as up.