How Much Do I Need Invested to Withdraw £1,000 a Month?

Reviewed 19 May 2026. A worked example for turning a monthly income goal into a rough pot target. It is deliberately simple so you can see the moving parts.

A £1,000-a-month target is useful because it is concrete. It could cover bills, bridge a gap before a pension starts, or add breathing room in retirement. The pot you need depends on tax, inflation and how much market wobble you can live with.

The rough calculation is straightforward: £1,000 a month is £12,000 a year. Divide that annual income by a withdrawal rate and you get a starting point.

| Withdrawal rate | Estimated pot for £1,000/month before tax | What it implies |

|---|---|---|

| 3.0% | £400,000 | More cautious starting point |

| 3.5% | £343,000 | Middle-ground planning estimate |

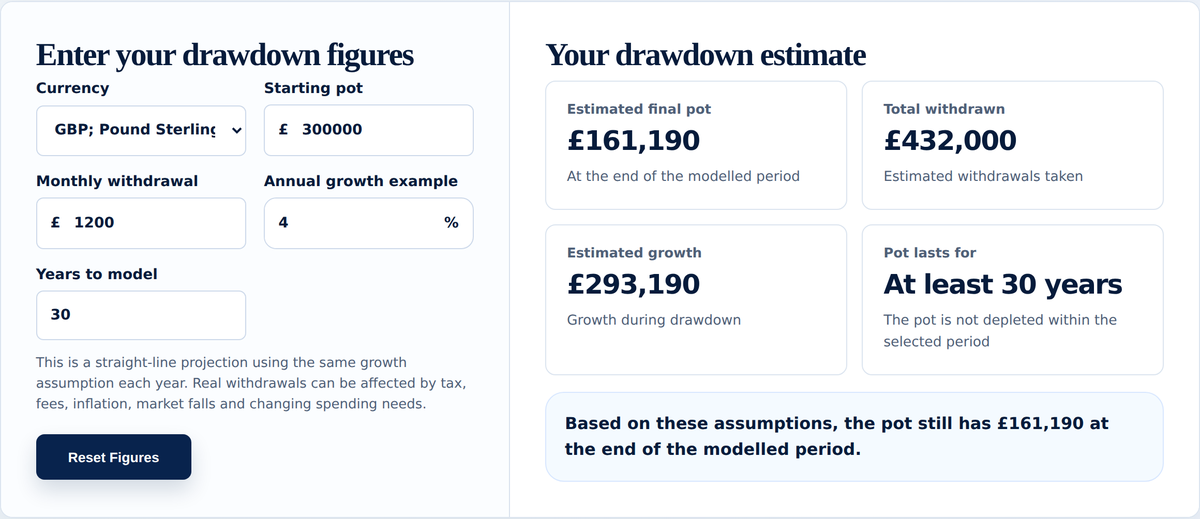

| 4.0% | £300,000 | Common rule-of-thumb, not a guarantee |

| 5.0% | £240,000 | More aggressive; higher risk of running down the pot |

These are before-tax income targets. A pension withdrawal, ISA withdrawal and general investment account withdrawal can have very different tax treatment.

Why £300,000 is not the whole answer

A £300,000 pot with a 4% withdrawal rate gives a first-year income of £12,000. But markets do not grow in straight lines. If poor returns arrive early in retirement, withdrawals can do more damage because you are selling units while the pot is down. This is called sequence risk.

Inflation also matters. £1,000 per month today will not buy the same lifestyle in 20 or 30 years. If you want income that keeps pace with inflation, your plan needs to allow withdrawals to rise over time.

ISA, pension and tax treatment

ISA withdrawals are normally tax-free. Pension withdrawals can be taxable, although many people can usually take up to 25% of eligible pension benefits as tax-free cash within the relevant rules and allowances. General investment accounts can involve dividend tax and Capital Gains Tax. That is why the same headline pot can support different after-tax spending depending on where the money sits.

Three quick examples

- £240,000 pot: £1,000/month requires a 5% withdrawal rate. This may work for some periods, but leaves less margin for weak markets.

- £300,000 pot: £1,000/month requires a 4% withdrawal rate. This is a common planning reference point, but still not guaranteed.

- £400,000 pot: £1,000/month requires a 3% withdrawal rate. This gives more room for caution, inflation and market shocks.

Use the calculator

Use the Drawdown Calculator to test your own withdrawal amount, inflation assumption and investment return. Use the Retirement Calculator if you are still building the pot.

Sources and assumptions

- GOV.UK: tax on pension income

- GOV.UK: Individual Savings Accounts

- GOV.UK: Capital Gains Tax rates and allowances

- Your Wealth Calculator methodology

Where to build the pot

Building an income-generating pot means choosing where to hold it, whether a stocks and shares ISA on an investment platform or a pension such as a SIPP. The Knowledge Hub covers choosing an ISA platform and what to look for in a SIPP provider.

This article is for general information only. It is not financial advice, pension advice, drawdown advice or a personal recommendation. The examples are here to help you understand the moving parts, but they cannot tell you what withdrawal rate or retirement plan is right for you.

Drawdown involves investment risk. The value of investments and any income from them can go down as well as up, and you may get back less than you put in. Poor market returns, inflation and taking too much too early can all affect how long a pension pot lasts. Consider qualified financial advice if you are unsure.