Mortgage Overpayment vs Investing at 3%, 4%, 5% and 6% Rates

Reviewed 19 May 2026. Uses a £500-a-month worked example to compare mortgage rates with possible investment returns. The certainty/risk trade-off is the point.

The mortgage-versus-investing question changes completely as the mortgage rate rises. At 3%, investing may look easier to justify in many models. At 6%, overpaying can start to look less like a conservative choice and more like a meaningful risk-free saving on mortgage interest.

This guide uses a simple scenario: £500 per month for 10 years. It compares the value of overpaying a mortgage at different interest rates with the return an investment would need to justify taking market risk.

Scenario: £500 per month for 10 years

Mortgage overpayment behaves like a saving equal to your mortgage interest rate, because every pound of debt repaid stops interest from being charged on that pound. The exact mortgage term and lender rules matter, but this comparison is a useful first screen.

| Scenario | Total paid in | Approx. value after 10 years | Interest avoided / growth | Investment hurdle |

|---|---|---|---|---|

| 3% mortgage rate | £60,000 | £69,871 | £9,871 | 3% after-tax return needed to beat it |

| 4% mortgage rate | £60,000 | £73,625 | £13,625 | 4% after-tax return needed to beat it |

| 5% mortgage rate | £60,000 | £77,641 | £17,641 | 5% after-tax return needed to beat it |

| 6% mortgage rate | £60,000 | £81,940 | £21,940 | 6% after-tax return needed to beat it |

For comparison, investing £500 per month for 10 years at a 5% annual return would grow to roughly £77,641 before fees and tax. That is more than overpaying at 3% or 4%, roughly similar to 5%, and lower than the certainty of overpaying at 6%.

Do not compare your mortgage rate with a headline investment return. Compare it with a realistic after-tax, after-fee, risk-adjusted investment return.

When overpaying starts to look very strong

At lower mortgage rates, investing has a better chance of coming out ahead over long periods, especially inside an ISA or pension. At higher mortgage rates, the interest saving from overpaying becomes harder to dismiss. A 6% mortgage overpayment is not the same as chasing a possible 6% market return. One reduces a known borrowing cost if your lender applies the overpayment correctly; the other is uncertain.

When investing can still make sense

Investing can still be sensible if you have a long time horizon, enough emergency cash, no expensive debt, and tax-efficient account space such as an ISA or pension. It can also keep money more accessible than mortgage overpayments, depending on the account used. The price of that flexibility is market risk.

What this simple table leaves out

- Overpayment charges or lender limits.

- Changes in mortgage rate at remortgage.

- Investment platform fees and fund charges.

- Tax on dividends, interest or capital gains outside an ISA or pension.

- The value of liquidity; money in an ISA is usually easier to access than money overpaid into a mortgage.

Run the comparison with your figures

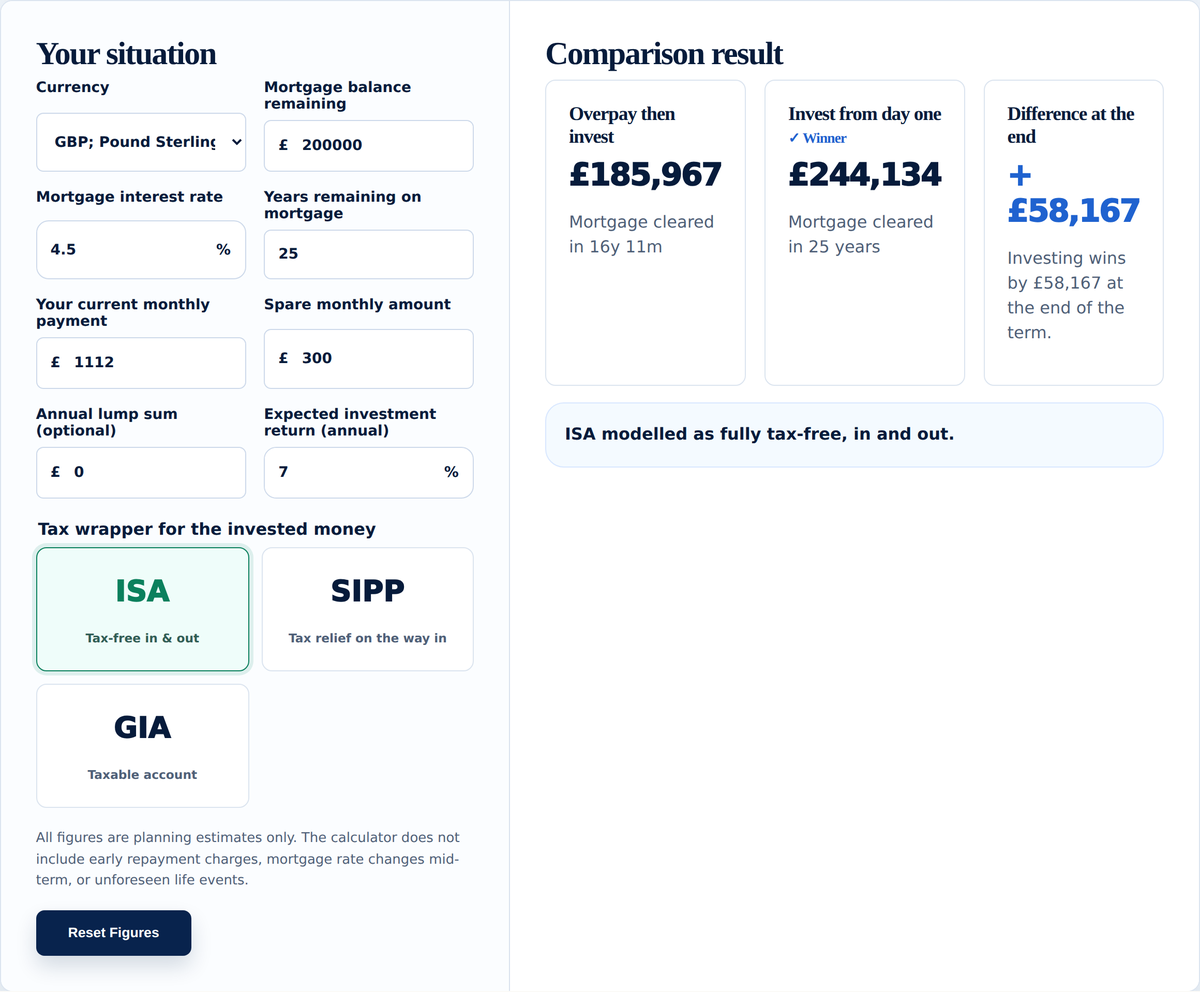

Use the Mortgage vs Invest Calculator to compare your mortgage rate, spare monthly cash, investment return assumption and tax wrapper. You can also use the Investment Calculator to test different return scenarios.

Sources and useful reading

- GOV.UK: Capital Gains Tax rates and allowances

- GOV.UK: Individual Savings Accounts

- Your Wealth Calculator methodology

If investing wins for you

If the numbers point you toward investing, the usual home for it is a stocks and shares ISA held on an investment platform. The Knowledge Hub covers how to choose one.

This article is for general information only. It is not financial advice, mortgage advice, investment advice or a personal recommendation. The examples are here to help you compare the trade-offs, but they cannot tell you whether overpaying, investing or doing both is right for your circumstances.

Mortgage overpayments may reduce flexibility, and investments involve risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns.