What Happens If I Salary Sacrifice Below £50,270?

Reviewed 19 May 2026. Uses England, Wales and Northern Ireland 2026/27 tax bands and employee National Insurance assumptions.

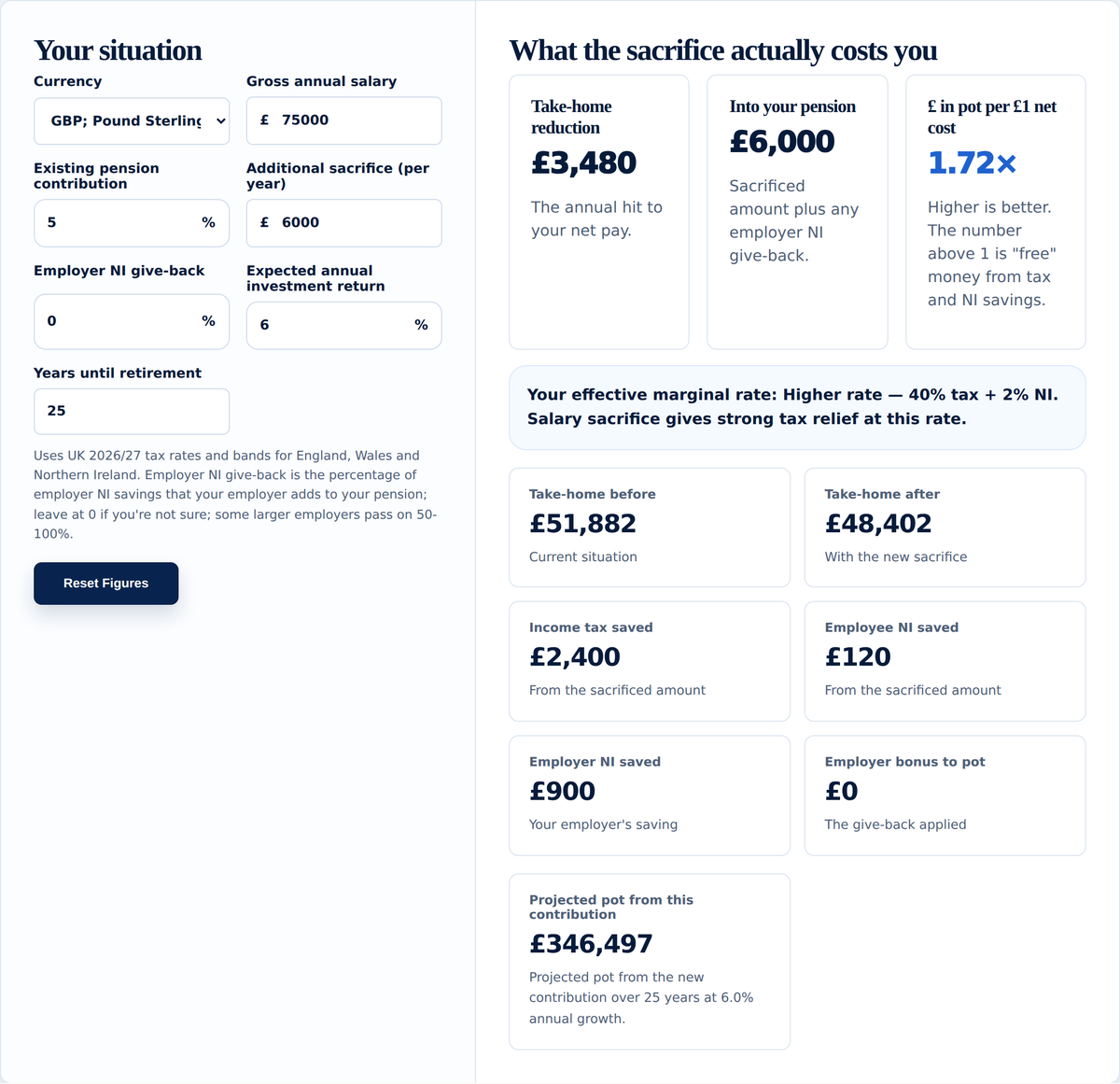

£50,270 matters because it is where the higher-rate Income Tax band currently starts for England, Wales and Northern Ireland taxpayers. That makes it a natural line to test when you are thinking about salary sacrifice.

Sacrificing income down to £50,270 can be efficient because the pounds above that line are usually exposed to 40% Income Tax and 2% employee National Insurance. It still needs care, because you are trading take-home pay today for pension money later.

Example: sacrificing down to the higher-rate threshold

The table below shows the estimated salary sacrifice needed to reduce gross pay to £50,270. It assumes England/Wales/Northern Ireland tax bands, employee Class 1 National Insurance, no student loan and no other taxable income. The final two columns show how the picture changes if an employer passes on a full 15% employer NI saving. Many employers pass on less or none.

| Gross salary | Sacrifice to reach £50,270 | Estimated take-home pay cost | Pension per £1 cost | If full 15% employer NI is added | Pension per £1 cost with give-back |

|---|---|---|---|---|---|

| £55,000 | £4,730 | £2,743 | 1.72x | £5,440 | 1.98x |

| £60,000 | £9,730 | £5,643 | 1.72x | £11,190 | 1.98x |

| £65,000 | £14,730 | £8,543 | 1.72x | £16,940 | 1.98x |

| £80,000 | £29,730 | £17,243 | 1.72x | £34,190 | 1.98x |

In this simplified model, every £1 sacrificed from the higher-rate band gives up about 58p of take-home pay and puts £1 into your pension. If your employer adds a full NI give-back, the pension value can approach £1.98 per £1 of take-home pay given up.

What about the 2029 salary sacrifice change?

GOV.UK has announced that from April 2029, only the first £2,000 of employee pension contributions through salary sacrifice each year will remain exempt from National Insurance. The Income Tax benefit is expected to remain, subject to the usual pension rules. That means the threshold strategy may still matter, but the NI part of the advantage could be smaller after the reform.

Reasons not to sacrifice all the way down

- You may need the cash for an emergency fund, house move, debt repayment or family costs.

- Your mortgage lender may look at your reduced contractual salary.

- Some employment benefits and statutory payments can be affected by lower salary.

- You might already be close to pension annual allowance issues.

- You may prefer ISA flexibility if you need access before pension age.

A sensible way to use the threshold

Rather than treating £50,270 as a magic number, use it as a planning checkpoint. Test three scenarios: your current contribution, a contribution that brings you partly down into the higher-rate band, and a contribution that gets you to around £50,270. Then compare the take-home pay cost against the pension value created.

Start with the Salary Sacrifice Calculator, then compare pension vs ISA flexibility in ISA vs pension for basic-rate and higher-rate taxpayers.

Sources and assumptions

- GOV.UK: Income Tax rates and bands

- GOV.UK: National Insurance thresholds 2026/27

- GOV.UK: salary sacrifice reform from April 2029

If your workplace scheme is limited

Salary sacrifice goes through your workplace pension. If its fund choice or charges are poor, a personal pension or SIPP can sit alongside it for extra contributions. The Knowledge Hub explains how that works.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. Salary sacrifice affects pay, pension contributions and tax treatment, so the right answer depends on your own situation and employer scheme.

Where pension investing is discussed, remember that investing involves risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns. Tax and pension rules can change.