Salary Sacrifice Examples at £40k, £50k, £60k, £80k and £100k

Reviewed 19 May 2026. Worked examples using a simple 10% salary sacrifice. Good for understanding the shape of the trade-off, not for replacing payroll figures.

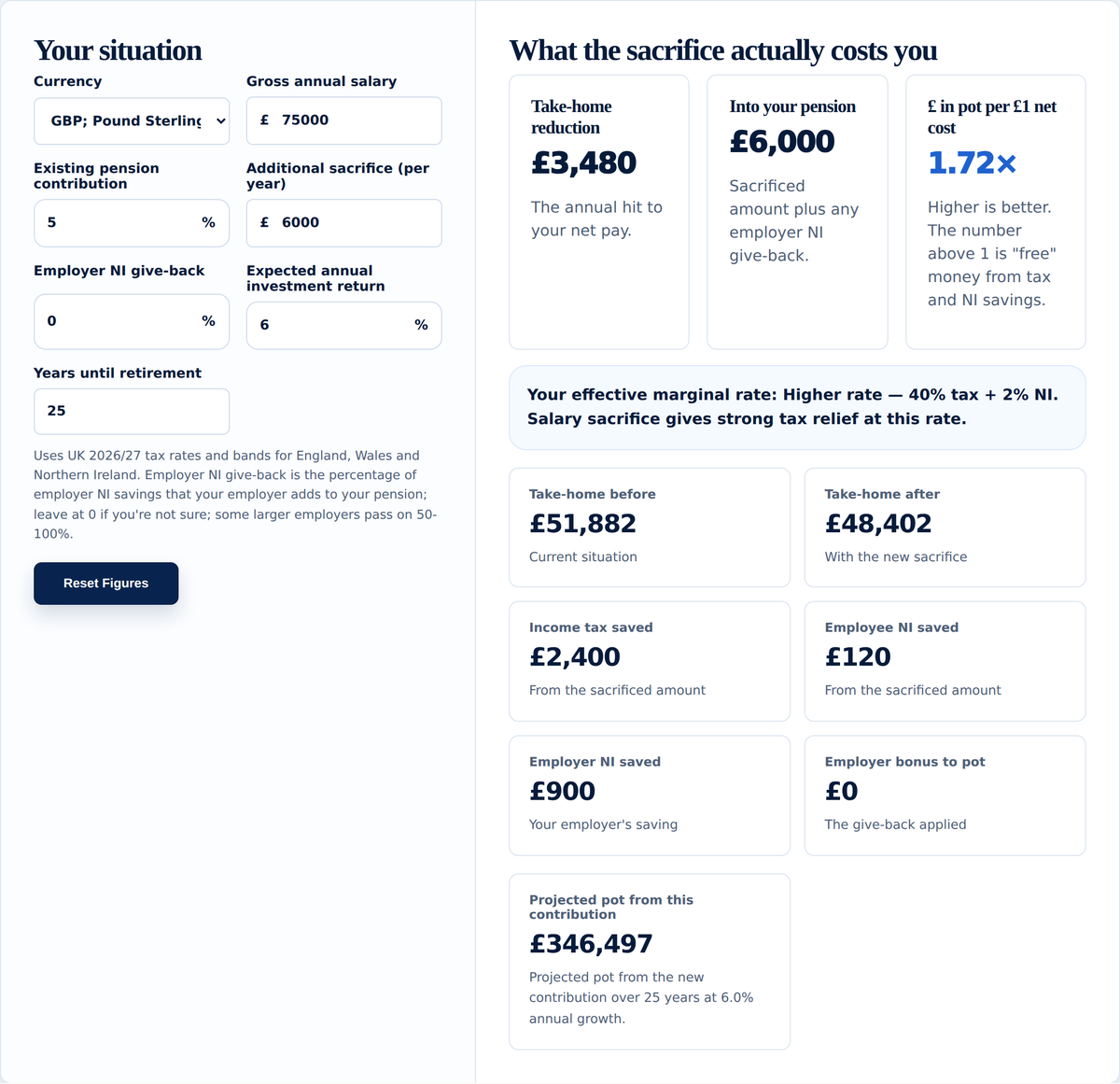

The headline benefit of salary sacrifice is easy to explain: more money goes into your pension than leaves your payslip. The practical question is: what does that trade-off actually look like at different income levels?

The examples below use a simple comparison: sacrifice 10% of gross salary into a pension, assume England/Wales/Northern Ireland Income Tax bands, employee Class 1 National Insurance, no student loan, no child benefit charge, no bonus and no employer NI give-back. Scotland has different Income Tax bands, so Scottish taxpayers should treat the figures as a framework rather than a direct estimate.

Look at the “take-home pay cost” column. That is the amount of spending power you give up. The pension contribution is larger because some of the money that would have gone to tax and NI goes into your pension instead.

| Gross salary | 10% sacrificed into pension | Estimated take-home pay cost | Income Tax saved | Employee NI saved | Pension per £1 take-home cost |

|---|---|---|---|---|---|

| £40,000 | £4,000 | £2,880 | £800 | £320 | 1.39x |

| £50,000 | £5,000 | £3,600 | £1,000 | £400 | 1.39x |

| £60,000 | £6,000 | £3,480 | £2,400 | £120 | 1.72x |

| £80,000 | £8,000 | £4,640 | £3,200 | £160 | 1.72x |

| £100,000 | £10,000 | £5,800 | £4,000 | £200 | 1.72x |

What the examples show

At £40,000 and £50,000, most of the sacrificed income would otherwise have been taxed at 20% Income Tax and 8% employee National Insurance. In this simplified model, that means each £1 into the pension costs roughly 72p of take-home pay.

At £60,000, £80,000 and £100,000, the sacrificed income is mainly in higher-rate territory. The saving is closer to 40% Income Tax plus 2% employee National Insurance, so each £1 into the pension costs roughly 58p of take-home pay before any employer NI give-back.

The figures can become more pronounced above £100,000 because of the Personal Allowance taper, but that deserves its own article because the marginal rate can be misleading if you do not define adjusted net income carefully.

Where employer NI give-back changes the answer

Some employers share part of the employer National Insurance saving. For 2026/27, the main employer NI rate is 15% above the secondary threshold. If an employer passes some of that saving into your pension, the pension contribution can be larger than the salary you sacrificed. Not every employer does this, and the percentage can vary, so the calculator lets you test it separately.

When this does not mean “sacrifice as much as possible”

Salary sacrifice can reduce your contractual salary. That can matter for mortgage affordability, some salary-linked benefits, statutory payments and short-term cashflow. Pension money is also locked away until at least minimum pension age, which is due to rise to 57 from April 2028 for most people.

Use the calculator with your own salary

Use the Salary Sacrifice Calculator to test your own salary, pension percentage and employer NI give-back. If you are close to a tax threshold, also read what happens if you salary sacrifice below £50,270 and how the 60% tax trap works.

Sources and assumptions

- GOV.UK: Income Tax rates and Personal Allowance

- GOV.UK: employer PAYE and National Insurance thresholds 2026/27

- GOV.UK: salary sacrifice reform from April 2029

- Your Wealth Calculator methodology

Common questions

Short answers to questions this example often raises.

Why does £60,000 look more efficient than £50,000?

Because the sacrificed income is mostly in higher-rate tax territory. The simplified saving is usually 40% Income Tax plus 2% employee NI, compared with 20% Income Tax plus 8% NI for much basic-rate income.

Does this include employer pension contributions?

No. The table only models the sacrificed employee salary. Employer contributions and employer NI give-back can make the pension outcome better.

Does this work the same in Scotland?

No. Scotland has different Income Tax bands. The broad principle is similar, but the exact numbers need Scottish tax assumptions.

Where larger contributions can go

If you want to contribute beyond what your workplace scheme offers, a personal pension or SIPP can run alongside it. The Knowledge Hub covers what to look for in a SIPP provider.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. Salary sacrifice affects pay, pension contributions and tax treatment, so the right answer depends on your own situation and employer scheme.

Where pension investing is discussed, remember that investing involves risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns. Tax and pension rules can change.