How Much Emergency Fund Do I Need in the UK?

Reviewed 19 May 2026. Built around UK emergency-savings guidance. The useful number is your own essential spending, not someone else’s headline target.

An emergency fund is not supposed to be impressive. It is there so a broken car, job wobble or surprise bill does not become expensive debt or a forced investment sale.

The common rule of thumb

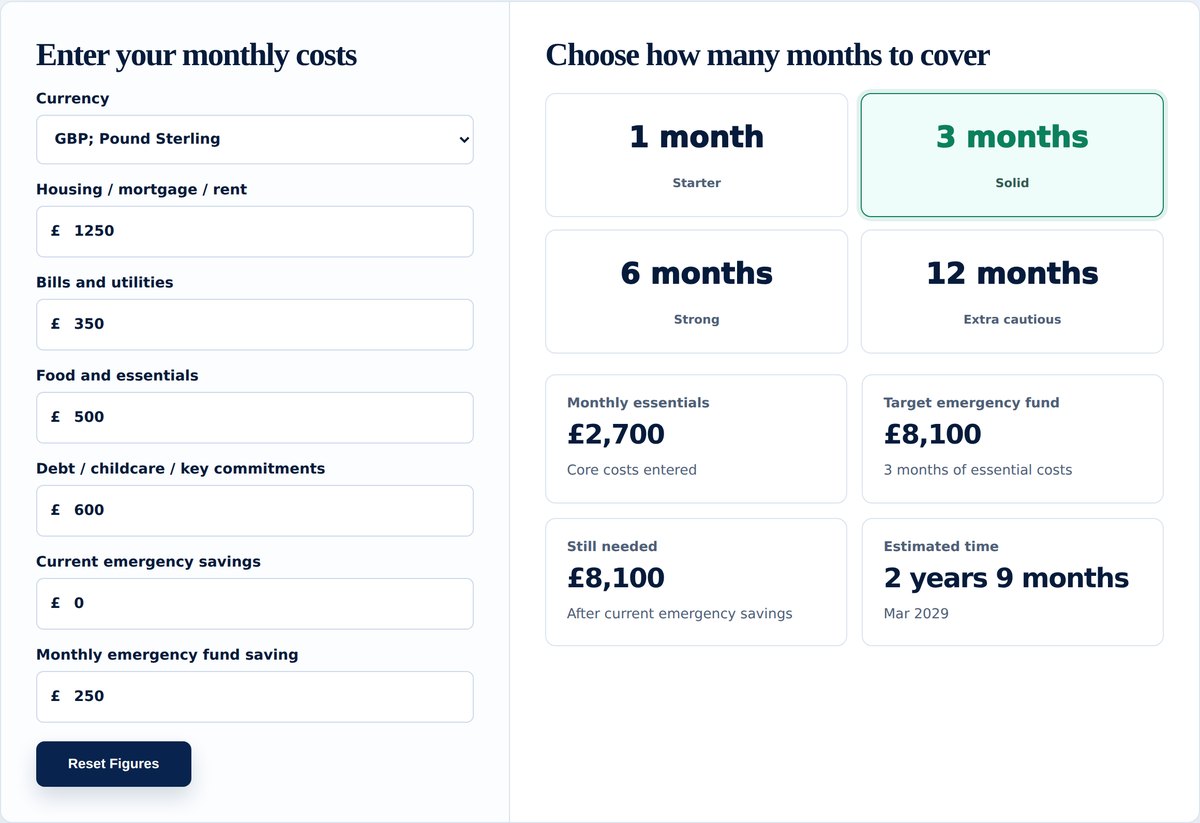

A common rule of thumb is three to six months of essential outgoings in an instant access savings account. That means essentials, not your full lifestyle spend.

What counts as essential spending?

- rent or mortgage;

- council tax and utilities;

- food and basic household costs;

- insurance;

- transport needed for work;

- minimum debt repayments;

- childcare or dependent costs.

When one to three months may be enough

A smaller fund may be reasonable if your income is secure, your expenses are low, you have no dependants, and you could temporarily cut spending quickly.

When six months or more makes sense

A larger fund can be sensible if you have dependants, irregular income, a mortgage, health concerns, an older car, self-employment income, or a job where finding another role could take time.

A £500 starter buffer can be a useful first layer while you build towards a fuller emergency fund over time.

Where should it be kept?

Emergency money is usually best kept accessible. If it is in investments, its value can fall just when you need it. If it is locked away, it may not help when the emergency arrives. The FSCS deposit protection limit rose to £120,000 per eligible person, per UK-authorised firm from 1 December 2025.

Use the calculator

The Emergency Fund Calculator lets you enter your real essential costs and compare different month targets.

Related guides

Sources and useful reading

Common questions

Quick answers to the questions that come up most.

Is three months enough emergency savings?

It can be enough for some people, especially with secure income and low fixed costs. Others may need six months or more.

Should my emergency fund be in cash or investments?

Usually cash, because the point is access and stability rather than long-term return.

Can a credit card replace an emergency fund?

A 0% card can help with liquidity, but it is still debt. Cash gives more control and avoids relying on credit availability during stress.

This article is for general information only. It is not financial advice or a personal recommendation. The examples are here to help you think through your own emergency fund, but they cannot tell you what is right for your circumstances.

Emergency money is usually held in cash because access and stability matter. Interest rates, inflation and tax rules can still change over time. If you choose to invest money instead, remember that investing involves risk and the value of investments can go down as well as up.