The ISA Bridge to Early Retirement

Reviewed 7 June 2026. A guide to using ISAs to fund the years before you can access your pension; not a recommendation or a personal plan. Figures reflect the 2026/27 UK tax year.

Pensions are the most tax-efficient way to save for later life, but they carry a catch that anyone retiring early runs straight into: you cannot touch the money until pension age. If you want to stop work before then, you need a different pot to live on in the meantime. That pot is the bridge, and for most people in the UK it is built inside a stocks and shares ISA.

The idea is simple once you see it. Work out how many years sit between when you want to stop and when your pension unlocks, fund those years from money you can actually reach, and let the pension keep growing untouched until it is allowed to pay out. Get the bridge right and early retirement becomes a question of arithmetic rather than luck.

Why early retirement needs a bridge

Pension money is locked until age 55, rising to 57 from April 2028. The State Pension comes later still, currently from 66 and rising to 67. So if you plan to stop work at, say, 52, there is a stretch of years where neither your pension nor the State Pension can help. Something has to cover your spending in that gap, and it has to be money you can withdraw freely. An ISA does exactly that, because you can take from it whenever you like and the withdrawals are tax-free.

How big should the bridge be?

Start with the years it has to cover. Take the age you want to retire, subtract it from your pension access age, and that is the length of the bridge. Multiply those years by your expected annual spending, then take off any other income you will have in that window, such as part-time work or rental income. That gives a rough size.

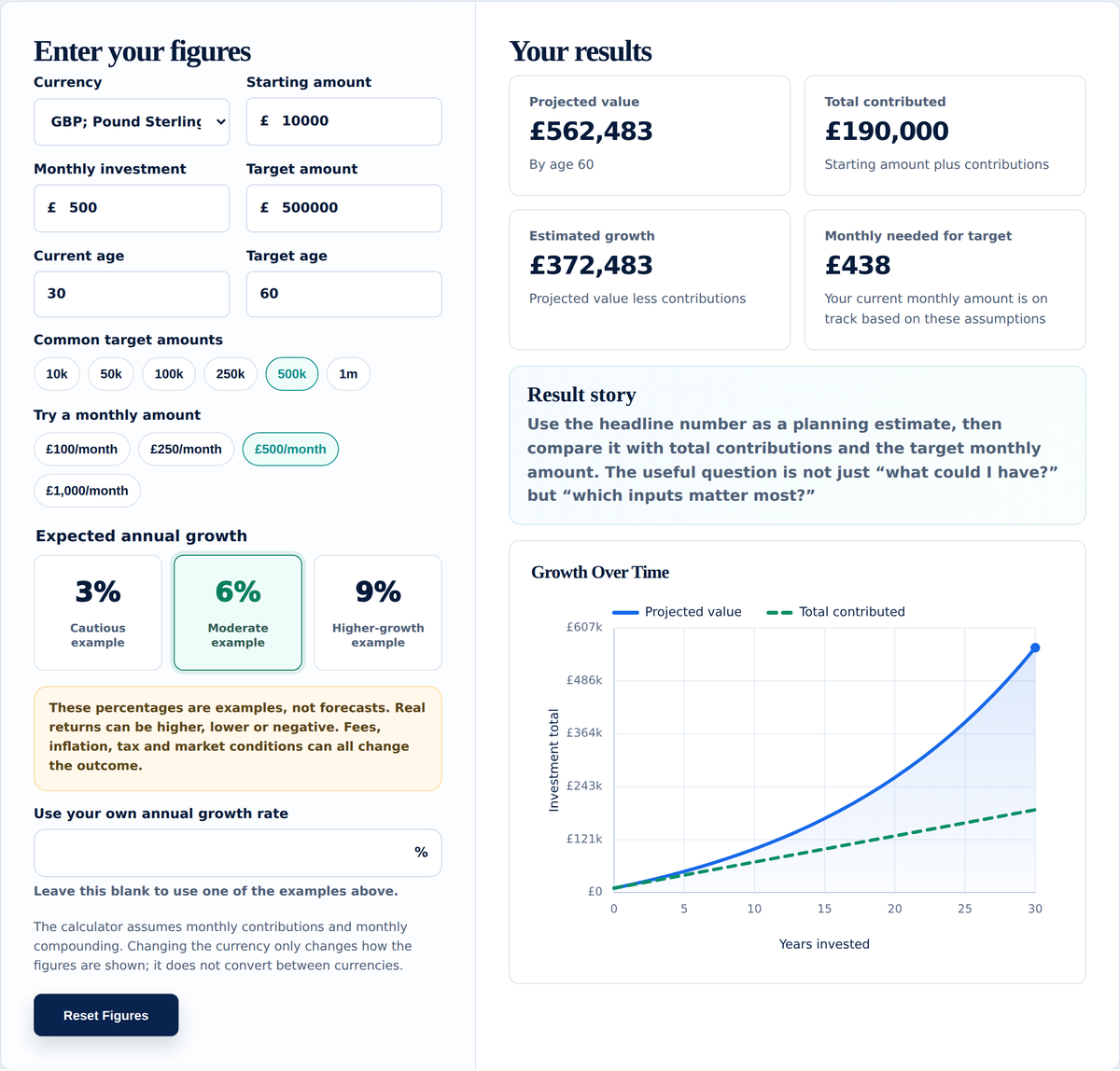

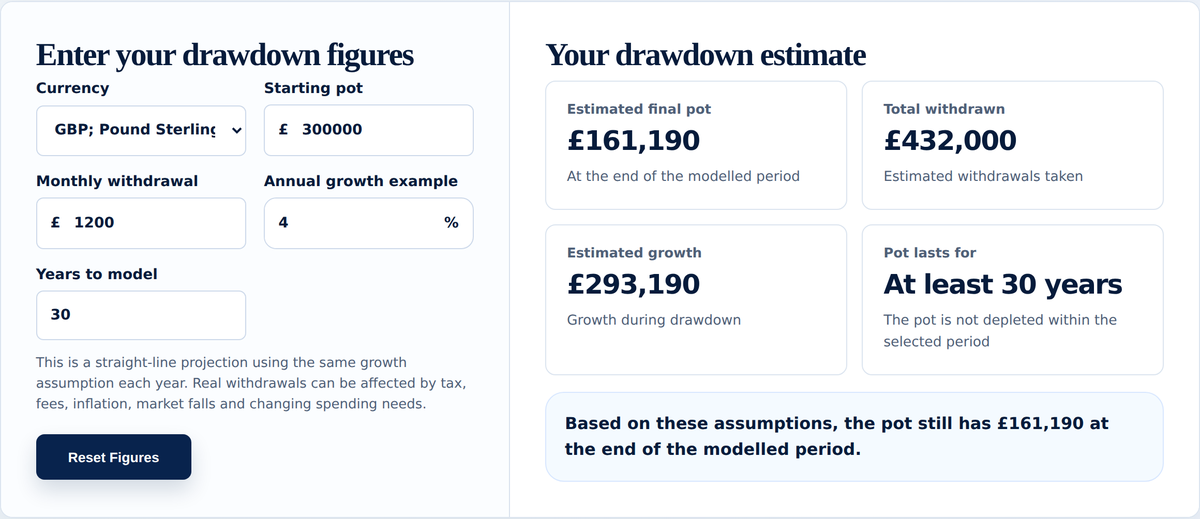

An example makes it concrete. Suppose you want to retire at 52 and your pension unlocks at 57. That is a five-year bridge. If you expect to spend £25,000 a year, the simple sum is £125,000. In practice you would want more, because prices rise over those years and because a poor run in markets early on can shrink the pot faster than planned. Treat the simple figure as a floor, not a target. The Investment Calculator shows what regular investing could build toward it, and the Drawdown Calculator models how a pot holds up as you draw it down.

Do not become pension-rich but access-poor

The most common early-retirement mistake is funnelling everything into the pension because the tax relief is so attractive, then realising the money cannot be reached until 57. You end up with a healthy pension and no way to pay the bills in the years before it unlocks. The opposite error is neglecting the pension entirely and giving up valuable relief. The skill is splitting your saving so the ISA bridge is large enough for the early years while the pension is still doing its long-term work. The order to think about this in is covered in which should come first, and how the relief changes by tax band in ISA vs pension for basic-rate and higher-rate taxpayers.

Where a Lifetime ISA fits

A Lifetime ISA is tempting for retirement because of its 25% bonus, but it has a catch of its own: the money is locked until age 60, with a charge for taking it out earlier. That means it cannot fund a bridge before 60. If you plan to retire at 60 or later it can form part of the plan, and it is useful for a first home, but for an earlier finish it does not solve the access problem the bridge exists to solve.

The order you spend things in retirement

Once retired, the sequence usually runs in stages. The ISA bridge covers the first years. When the pension unlocks, you switch to drawing from it, often taking some of the 25% tax-free element to keep your taxable income low. Later, the State Pension joins from your late sixties. Blending these, rather than emptying one before starting the next, can keep more of your income out of tax. The guides on how long a pension might last and how much you need to withdraw a set income go into the pension stage.

The risk to watch

A bridge is drawn down over a short window, so it is more exposed to bad timing than a pot meant to last thirty years. A market fall in the first year or two of a five-year bridge can do real damage, because there is little time to recover before the money is spent. Holding the cash you will need soonest in lower-risk assets, rather than leaving the whole bridge in shares, reduces that danger. It also means the popular 4% rule is the wrong tool here; that rule is built for long retirements, while a short bridge is closer to working out a known number of years of spending.

Test it with your own numbers

The Investment Calculator projects how the bridge could be built, the Drawdown Calculator shows how it holds up as you spend it, the Retirement Calculator checks the pension side, and the ISA vs Pension Calculator helps you balance contributions between the two. The Wealth Planner brings the whole picture together.

Related guides

- ISA vs pension: which should come first?

- ISA vs pension for basic-rate and higher-rate taxpayers

- Should I overpay my mortgage or pay into my pension?

- How long will my pension last?

Sources and useful reading

- GOV.UK: Individual Savings Accounts

- GOV.UK: Lifetime ISA

- GOV.UK: when you can take your pension

- GOV.UK: State Pension age

- Your Wealth Calculator: methodology and assumptions

Common questions

Questions people often have about funding an early retirement.

What is an ISA bridge?

An ISA bridge is an accessible pot, usually held in a stocks and shares ISA, that funds the years between stopping work early and the age at which you can access your pension. It bridges the gap that a pension alone cannot cover, because pension money is locked until at least 55, rising to 57 in 2028.

How big should my ISA bridge be?

Roughly the number of years between your planned early-retirement age and your pension access age, multiplied by your annual spending, less any other income in those years. Add a margin for inflation and poor markets, so the real figure is usually higher than the simple sum.

Can I retire before I can access my pension?

Yes, but only if you have savings you can actually reach in the meantime, since the pension stays locked until pension age. That accessible pot is the bridge, and for most people it sits in an ISA.

Does a Lifetime ISA work as a bridge?

Only partly. A Lifetime ISA adds a 25% bonus but is locked until age 60, with a charge for taking it out earlier, so it cannot fund a bridge before 60. It can help the part of an early retirement that falls at 60 or later, but not the years before that.

Should I use an ISA or a pension for early retirement?

Both, in balance. The pension gives the strongest tax relief for the long term, while the ISA gives the access you need in the early years. Funding only the pension can leave you pension-rich but unable to reach the money when you stop work.

When can I access my pension?

Not until age 55 at the earliest, rising to 57 from April 2028. The State Pension comes much later, currently from age 66 and rising to 67, which is why an early retirement often needs both an ISA bridge and a plan for the pension and State Pension that follow.

How do I avoid running out during the bridge years?

Size the bridge with a margin, keep the money you will spend soonest in lower-risk assets, and revisit the plan as markets move. A bridge is drawn down over a short window, so a poor run early on matters more than it would over a long retirement.

Is the 4% rule the right way to size a bridge?

Not really. The 4% rule is built around a retirement lasting about 30 years, while a bridge usually covers only a handful. A short, fixed window is closer to working out a known number of years of spending than applying a long-term withdrawal rate.

If you are building the bridge

A bridge is normally built inside a stocks and shares ISA, and the pension behind it through a workplace scheme or a SIPP. The Knowledge Hub covers how to start investing, choosing an ISA platform and what to look for in a SIPP provider.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. The examples are here to help you understand the trade-offs and do your own research.

Investing involves risk. The value of investments and any income from them can go down as well as up, and a pot drawn down over a short period is particularly exposed to poor timing. You may get back less than you put in. Pension access ages, ISA rules and tax allowances depend on your circumstances and may change.