ISA vs Pension: Which Should Come First?

Reviewed 7 June 2026. A guide to the order in which most people fill an ISA and a pension; not a recommendation to do either. Figures reflect the 2026/27 UK tax year.

ISAs and pensions are not really rivals. They solve different problems, and a strong plan usually uses both. The more useful question is not which is better, but which to feed first when you only have so much to put away each month. That order matters more than the wrapper itself.

The short version: a few foundations come before either, then the employer match, and only after that does the personal ISA-or-pension split really begin. This guide sets out that order and the handful of things that shift it.

The simple difference

An ISA is flexible. You can usually reach the money whenever you want, and growth and income inside it are tax-free. A pension is less flexible but usually more tax-efficient, because contributions attract tax relief, though the money is locked until pension age. How much that relief is worth depends on your tax band, which is covered in ISA vs pension for basic-rate and higher-rate taxpayers. How the access lock plays out for an early retirement is covered in the ISA bridge to early retirement. This guide stays on the order you fill them.

Start with the order, not the wrapper

For most people the first steps are the same whatever their tax band:

- Build an emergency fund, so a surprise bill does not force you into expensive borrowing. The Emergency Fund Calculator helps you size one.

- Clear expensive debt, such as a credit card balance, since that interest rate is almost always higher than a return you would expect from saving.

- Contribute enough to get the full employer pension match. This is the step people most often skip, and it is usually the best return available.

- Then decide how to split further money between an ISA and extra pension saving.

The match earns its place at the top. If your employer adds 5% when you add 5%, that matched portion is an immediate 100% on your money before any tax relief or growth. No ISA can match that, which is why giving up the match to feed an ISA is usually a mistake.

When the ISA earns priority

- You may need the money before pension age.

- You are building a house deposit or another medium-term goal.

- You already contribute enough to collect the full employer match.

- You value access more than squeezing out every last bit of tax efficiency.

When the pension earns priority

- Your employer matches contributions and you are not yet getting the full match.

- You are a higher-rate or additional-rate taxpayer, so the relief is larger.

- Your income sits between £100,000 and £125,140, where the Personal Allowance taper makes pension contributions especially valuable; see the 60% tax trap.

- You are clearly saving for retirement and will not need the money before pension age.

What about a Lifetime ISA?

A Lifetime ISA sits between the two. It adds a 25% government bonus, similar to a basic-rate top-up, but the money is locked until age 60 unless it goes toward a first home, and there is a charge for taking it out early. That makes it useful for a first property or for the later part of an early-retirement plan, rather than as your flexible, reach-it-anytime pot.

Allowances to know (2026/27)

- ISA allowance: £20,000 across your ISAs.

- Pension annual allowance: £60,000 for most people, lower for very high earners or where the £10,000 Money Purchase Annual Allowance applies.

- Pension access age: 55, rising to 57 from April 2028.

Test it with your own numbers

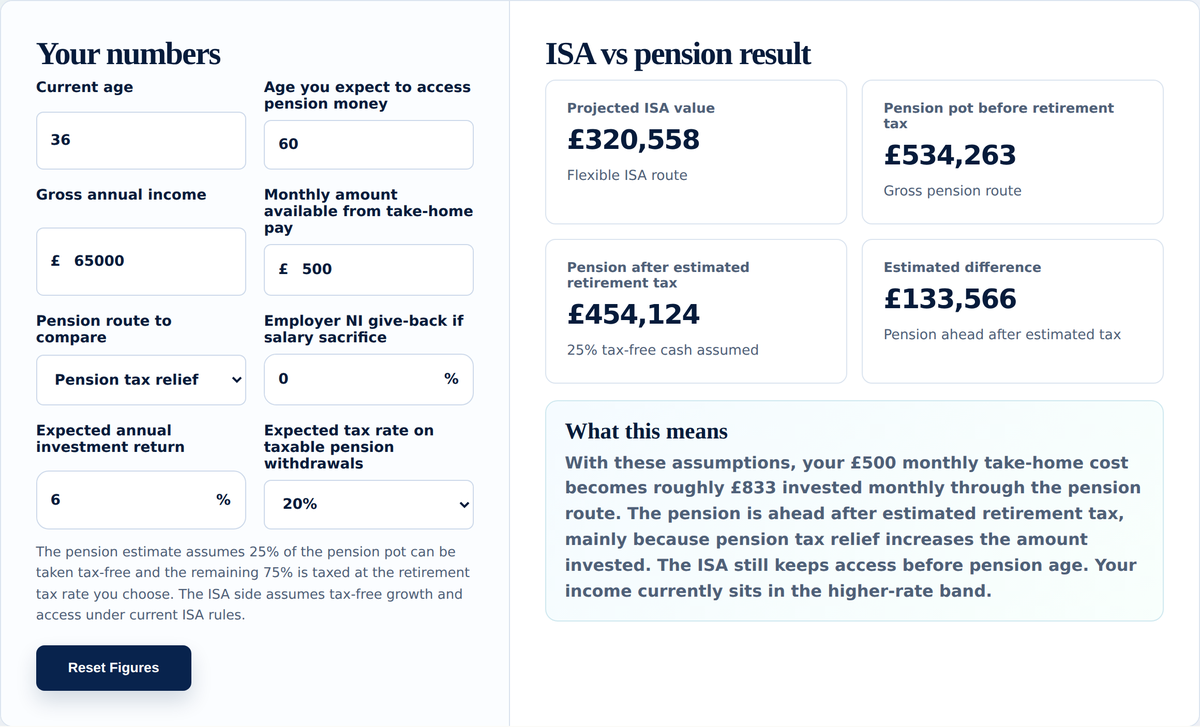

The ISA vs Pension Calculator compares the same contribution through each wrapper. The Salary Sacrifice Calculator shows how much pension relief is worth from your pay, the Investment Calculator models long-term growth, and the Retirement Calculator checks whether your retirement saving looks on track.

Related guides

- ISA vs pension for basic-rate and higher-rate taxpayers

- The ISA bridge to early retirement

- Should I overpay my mortgage or pay into my pension?

- How much should I invest each month?

Sources and useful reading

- GOV.UK: Individual Savings Accounts

- GOV.UK: tax relief on private pension contributions

- GOV.UK: when you can take your pension

- Your Wealth Calculator: methodology and assumptions

Common questions

A few of the questions this decision tends to raise.

Should I fill my ISA or pension first?

Usually neither comes before an emergency fund and the full employer pension match. After those, an ISA tends to come first if you may need the money before pension age, and a pension if you are a higher-rate taxpayer saving specifically for retirement.

Is it worth using an ISA if I get pension tax relief?

Yes, for money you might need before pension age. Relief is valuable, but it is no use if the money is locked away when you need it. Many people use a pension for retirement and an ISA for accessible medium-term wealth.

Should I stop my pension to build an ISA?

Rarely, and almost never to the point of losing an employer match. The match is usually the highest-return part of the whole plan.

Can I pay into both an ISA and a pension in the same year?

Yes. You can use both in the same tax year, up to £20,000 across your ISAs and up to your pension annual allowance.

Where does a Lifetime ISA fit?

It adds a 25% bonus but is locked until age 60 unless used for a first home, so it suits a first property or the later years of an early-retirement plan rather than your flexible pot.

Does the order change for higher earners?

It can. Higher-rate and additional-rate taxpayers get more from pension relief, and those in the £100,000 to £125,140 band gain the most, so the pension often moves up the order.

Where each one is opened

Whichever you prioritise, you open it somewhere: a stocks and shares ISA through an investment platform, or a pension through a workplace scheme or a personal SIPP. The Knowledge Hub covers choosing an ISA platform and what to look for in a SIPP provider.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. The numbers and examples are here to help you understand the trade-offs and do your own research. They cannot tell you what is right for your circumstances.

Investing involves risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns. Pension and tax rules and allowances depend on your circumstances and may change.