Should I Overpay My Mortgage or Pay Into My Pension?

Reviewed 7 June 2026. A decision guide for weighing a guaranteed mortgage saving against the tax-relief boost of a pension; not a recommendation to do either. Figures reflect the 2026/27 UK tax year.

This is the version of the overpay-or-invest question with the most lopsided maths and the biggest catch. A pension comes with tax relief, a guaranteed uplift on the way in that no mortgage overpayment can match. It also locks your money away until pension age. So the honest answer balances a near-certain head start against a long wait.

Here is the shape of it. Overpaying saves you your mortgage rate, guaranteed and tax-free, and the money becomes hard to reach again. Paying into a pension gives you an immediate, guaranteed boost from tax relief, then an uncertain market return on top, then a tax bill on most of it when you draw it. The relief is usually large enough to tilt the numbers toward the pension. The real question is whether the lock-up and the uncertainty are worth it for you.

The tax relief head start

Tax relief is what makes the pension so hard to beat. A £100 pension contribution costs a basic-rate taxpayer about £80 of take-home pay, because 20% relief is added on top. For a higher-rate taxpayer it costs about £60 once the extra relief is claimed, and for an additional-rate taxpayer about £55.

Turn that around and the advantage is obvious. A higher-rate taxpayer turns £60 of take-home pay into £100 working for them straight away, an uplift of roughly two-thirds before a penny of growth. A mortgage overpayment gives you your mortgage rate and nothing more. Even a 5% mortgage, which is a strong guaranteed saving by recent standards, cannot compete with an instant uplift of that size.

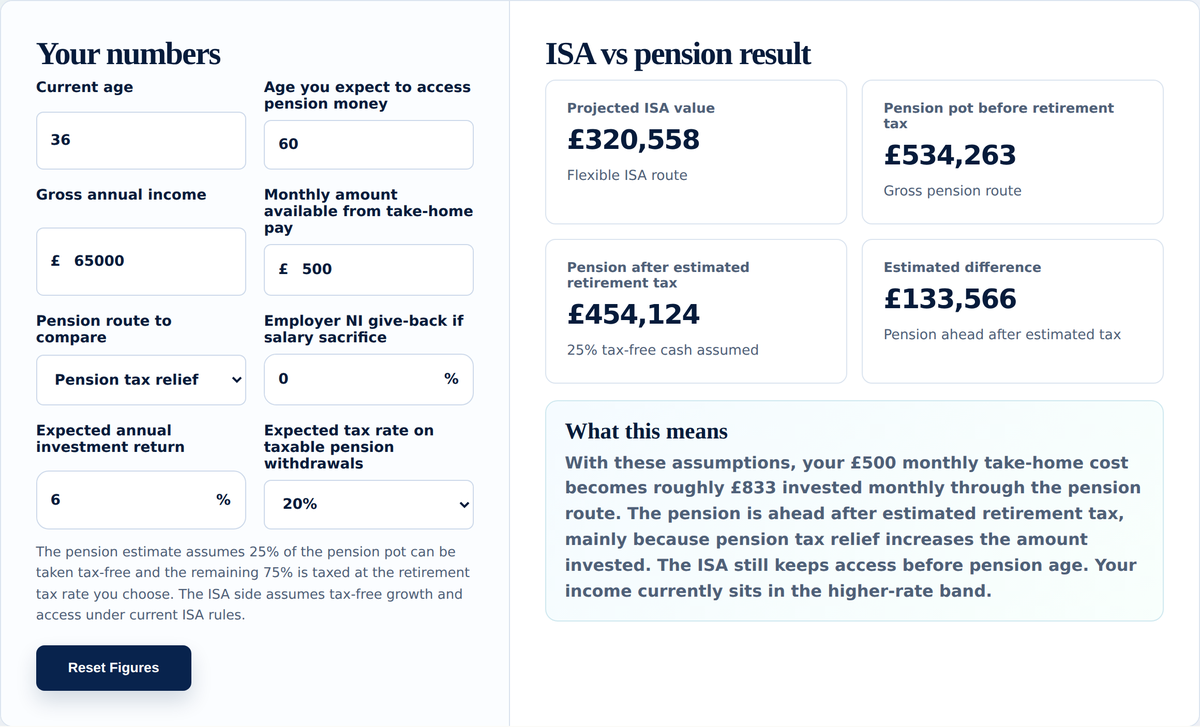

There is a genuine offset to weigh. Most of the pension is taxed when you take it out: 25% is normally tax-free and the rest is taxed at your marginal rate in retirement. So you do not keep the full relief. Even so, many people pay a lower rate in retirement than while working, and the tax-free portion plus years of sheltered growth usually leave the pension ahead on the numbers.

The employer match comes first

Before any of this, check your workplace pension. If your employer adds money when you contribute, that match is often an instant 100% return on the matched portion, which beats overpaying and ordinary investing comfortably. Take the full match first, then weigh overpaying against any extra pension saving. It is also worth having an emergency fund in place before you lock money away, so a bad month does not force you into expensive borrowing.

Salary sacrifice can widen the gap

If you can contribute by salary sacrifice, the pension pulls further ahead. Sacrifice saves National Insurance as well as Income Tax, and some employers pass on part of their own National Insurance saving too, so each pound stretches further than relief alone. The Salary Sacrifice Calculator shows the effect on your take-home pay.

There is one situation where the pension wins by a distance. If your income falls between £100,000 and £125,140, your Personal Allowance is tapered away, which creates an effective tax rate of around 60% on that slice of income. A pension contribution reduces the income that taper is measured against, so it can claw back the lost allowance, and the effective relief becomes exceptional. The guide to the 60% tax trap explains how that works.

The catch: you cannot touch it for years

Pension money is locked away until age 55, rising to 57 from April 2028. If there is a realistic chance you will need this money before then, the pension is the wrong home for it, and overpaying or an ISA keeps you flexible. A mortgage overpayment is also hard to reverse, but clearing the mortgage removes a monthly cost and gives you the home outright sooner, which is its own kind of security. The pension wins on growth and tax; the mortgage wins on certainty and on easing your monthly budget now.

A worked example

Say you are a higher-rate taxpayer with £200 a month of take-home pay to spare, and a mortgage at 5%. Put that £200 toward the mortgage and you save 5% interest, guaranteed, and chip steadily at the balance. Put the same £200 into a pension and, with higher-rate relief, it becomes around £333 invested before any growth at all. You have started from roughly a third more than you put in, and most of it then compounds tax-free for decades. The mortgage saving is certain, but it is small next to that head start. The price is that you cannot reach the pension until at least 55, rising to 57, while the mortgage saving improves your position straight away.

When overpaying often looks stronger

- You may need the money before pension age, so a long lock-up does not suit you.

- Your mortgage rate is high, so the guaranteed saving is large.

- You are close to clearing the mortgage and want the monthly payment gone.

- Carrying debt weighs on you, and a smaller mortgage would help you sleep.

- You have already secured your employer match and built an emergency fund.

When the pension often looks stronger

- You can comfortably leave the money untouched until pension age.

- You are a higher-rate or additional-rate taxpayer, so the relief is large.

- Your employer matches contributions, or you can use salary sacrifice.

- Your income sits between £100,000 and £125,140, where relief is exceptional.

- Your mortgage rate is modest, so the guaranteed saving is a low bar to clear.

For most people the sequence is the same. Build an emergency fund, clear expensive debt, take the full employer pension match, then weigh extra pension saving against overpaying. Matched money and tax relief are hard to beat, but they only help once the earlier foundations are in place.

What the maths leaves out

A paid-off home changes your retirement sums. Clearing the mortgage lowers your essential outgoings, which lowers how much income you need later. That is a quieter benefit than tax relief, but a real one.

Certainty has value. Some people simply sleep better with a smaller mortgage, and that is a fair reason to lean toward overpaying even when the pension edges it on paper.

Rules can change. Tax relief, the access age and the annual allowance have all moved before and may move again, so it is worth revisiting this rather than treating today's answer as fixed.

Test it with your own numbers

The Mortgage vs Invest Calculator compares overpaying against pension investing when you set the investment side to pension or SIPP and choose your tax band. The ISA vs Pension Calculator shows how the relief and the 25% tax-free, 75% taxable split work out, and the Investment Calculator lets you test how different growth assumptions change the pension side.

See how it fits your bigger picture

This choice is one part of a wider position that includes your savings, your other goals and your overall pension. The Net Worth Calculator shows where you stand today, and the Wealth Planner projects how your overall wealth could change, which helps you judge whether clearing debt or building the pension does more for where you are heading.

Related guides

- Should I overpay my mortgage or invest?

- Where overpaying your mortgage actually wins

- Mortgage overpayment vs investing at 3, 4, 5 and 6 percent

- ISA vs pension: which should come first?

- The ISA bridge to early retirement

- Is salary sacrifice worth it?

Sources and useful reading

- GOV.UK: tax relief on private pension contributions

- GOV.UK: when and how you can take your pension

- GOV.UK: Income Tax rates and Personal Allowance

- Your Wealth Calculator: methodology and assumptions

Common questions

Questions people often have before they decide.

Is it better to overpay my mortgage or pay into a pension?

On the numbers a pension often wins, because tax relief gives you an immediate, guaranteed uplift that no mortgage overpayment can match, and any employer match adds more. The trade-off is access: pension money is locked until at least age 55, rising to 57 in 2028. Overpaying wins on certainty and on freeing up your monthly budget sooner.

How much is pension tax relief worth?

A £100 pension contribution costs a basic-rate taxpayer about £80 of take-home pay, and a higher-rate taxpayer about £60 once the extra relief is claimed. Looked at the other way, a higher-rate taxpayer turns £60 into £100 invested straight away, an uplift no mortgage rate can rival. Most of the pension is taxed when you draw it, though 25% is normally tax-free.

Should I take my employer pension match before overpaying my mortgage?

Almost always, yes. An employer match is often an instant 100% return on the matched amount, which beats both overpaying and ordinary investing. Take the full match first, then weigh overpaying against extra pension saving.

When can I access my pension?

Not until age 55 at the earliest, rising to 57 from April 2028. If there is a realistic chance you will need the money before then, a pension is the wrong home for it, and overpaying or an ISA keeps you flexible.

Does paying into a pension help with the 60% tax trap?

Yes. Between £100,000 and £125,140 the Personal Allowance is tapered away, creating an effective 60% tax rate. A pension contribution reduces your adjusted net income, so it can claw back that allowance and the relief in this band is exceptional. In that situation the pension usually wins decisively over overpaying.

Is overpaying my mortgage safer than a pension?

The interest saving from overpaying is certain, while a pension carries market risk. But overpaying is not free of downsides either: the money is hard to get back, and you give up the tax relief and long-term growth a pension offers. Safer on the numbers is not the same as better for your goals.

Should I do both?

Many people do, and splitting your spare money can be both sensible and easier to stick to. A common approach is to secure the employer match and an emergency fund, then divide what is left between extra pension saving and overpaying, keeping some growth and some certainty.

Does salary sacrifice change the maths?

It can widen the pension's advantage. Contributing by salary sacrifice saves National Insurance as well as Income Tax, and some employers add part of their own NI saving too, so each pound stretches further than tax relief alone.

If you decide to use a pension

If you decide the pension is the better home for your spare money and your workplace scheme is limited, you may want a personal pension or SIPP of your own. The Knowledge Hub covers what to look for in a SIPP provider, opening a personal pension when your workplace scheme is limited, and how to consolidate old pension pots.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. The examples are here to help you compare the trade-offs, but they cannot tell you what is right for your circumstances.

Pension tax relief depends on your individual circumstances and may change. Pension money cannot normally be accessed until age 55, rising to 57 from April 2028. Investments can go down as well as up, and you may get back less than you put in. Mortgage overpayments may reduce your flexibility, and some deals limit how much you can overpay without a charge.