Is Salary Sacrifice Worth It?

Reviewed 4 June 2026. A UK pension salary-sacrifice guide, updated for the April 2029 National Insurance cap. Check your employer rules and payslip treatment before relying on the numbers.

Salary sacrifice has long been one of the most efficient ways to build a pension, because the amount landing in your pension can be larger than the take-home pay you give up to fund it. The reason so many people are asking whether it is still worth it is the November 2025 Budget, which introduced a National Insurance cap on sacrificed pension contributions from April 2029.

The short version: for most people salary sacrifice remains worth doing, and nothing changes at all before April 2029. What changes after that is narrower than the headlines suggest, and this guide walks through who is affected and by how much.

How salary sacrifice actually works

In a salary sacrifice arrangement, you formally agree to a lower contractual salary, and your employer pays the difference straight into your pension. Because those pounds never count as salary, they currently avoid both Income Tax and National Insurance, for you and often for your employer too. That is what makes it more efficient than paying into a pension from money that has already been taxed. It has to be a real change to your employment contract, not just a relabelling on your payslip, for HMRC to treat it as salary sacrifice.

Why it can be so efficient

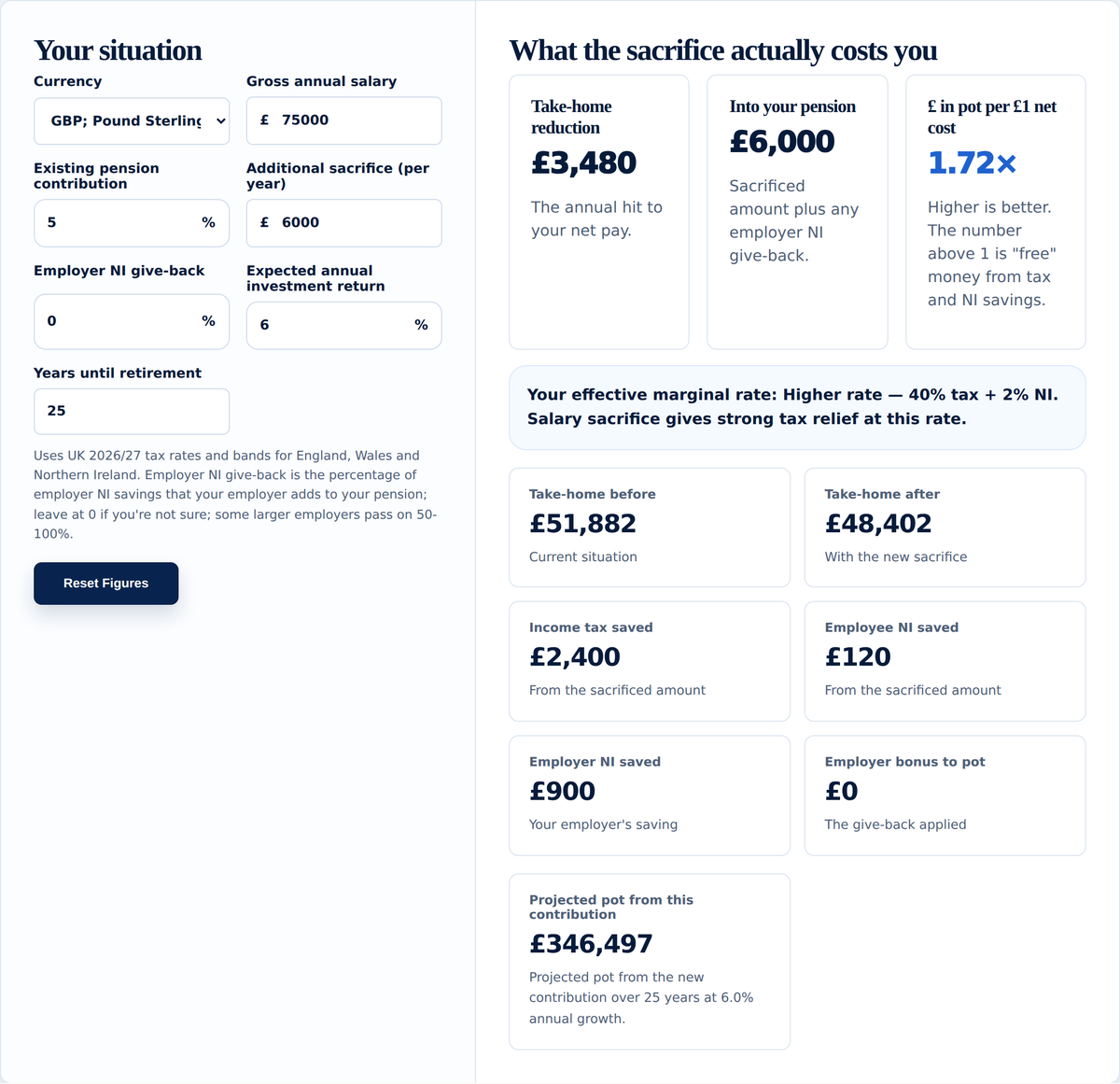

Under the current rules, sacrificing salary into your pension can save Income Tax at your marginal rate and employee National Insurance, and some employers add part of their own National Insurance saving on top. That stacking is why the value per pound can be high. A higher-rate taxpayer who gives up £100 of take-home pay can often end up with noticeably more than £100 in their pension once the tax and National Insurance savings are counted. The Salary Sacrifice Calculator shows this as the value per £1 of net pay sacrificed, alongside the reduction to your take-home pay.

Do not judge salary sacrifice by the size of the pension contribution on its own. Judge it by the pension contribution compared with the take-home pay you actually give up. That ratio is the real measure of how hard your money is working.

The April 2029 change: what is actually happening

At the November 2025 Budget, the government announced that from 6 April 2029 the National Insurance exemption on salary-sacrificed pension contributions will be capped at £2,000 per person per tax year. The change is being brought in through the National Insurance Contributions (Employer Pensions Contributions) Bill. In plain terms:

- The first £2,000 you sacrifice into your pension each year is unaffected. It keeps its full National Insurance exemption, exactly as now.

- Anything you sacrifice above £2,000 in a year loses that exemption. The excess is treated like ordinary earnings for National Insurance, so both you and your employer pay National Insurance on it.

- Income Tax relief is not changing. Above the cap you still receive full Income Tax relief on your pension contributions, and ordinary employer contributions made outside salary sacrifice stay free of National Insurance.

For the employee, National Insurance on the excess is charged at the normal rate, currently 8% on earnings between roughly £12,570 and £50,270 and 2% above that. For the employer it is 15%. So the people most affected are those sacrificing well over £2,000 a year, which usually means middle and higher earners putting a decent share of their salary into a pension.

Someone earning £50,000 who sacrifices 10% of their salary puts £5,000 a year into their pension. The first £2,000 keeps its National Insurance exemption; the remaining £3,000 does not. Based on current rates, that adds roughly £240 a year to their own National Insurance (8% of £3,000) and about £450 for their employer (15% of £3,000). Their Income Tax relief is untouched, and the full £5,000 still goes into the pension. Someone sacrificing £2,000 or less a year sees no change.

So is it still worth it after 2029?

For most people, yes, though the answer depends on how much you sacrifice.

If you sacrifice £2,000 a year or less, nothing changes. The arrangement is as efficient in 2029 as it is today. If you sacrifice more, you lose only the National Insurance slice on the amount above £2,000, not the Income Tax relief, which is usually the larger benefit. A higher-rate taxpayer keeps 40% Income Tax relief on the whole contribution either way, so salary sacrifice above the cap becomes about as efficient as a normal pension contribution, rather than pointless.

There are also reasons to use salary sacrifice that the change does not touch. Reducing your taxable salary can keep your income under £100,000, where the Personal Allowance starts to be withdrawn and the effective tax rate jumps. Our guide to the 60% tax trap explains how that works. It can also help with the High Income Child Benefit Charge. Those benefits come from the Income Tax side, which is unchanged.

Who tends to benefit most

- Higher-rate taxpayers: the Income Tax relief alone makes it efficient, before any National Insurance saving.

- People near £100,000: sacrificing salary can protect the Personal Allowance and sidestep the 60% trap.

- Employees whose employer shares its National Insurance saving: this adds pension value at no extra cost to you, and applies to the first £2,000 even after 2029.

- Long-term savers: pension money is locked away, so it suits retirement rather than goals you need to fund sooner.

When it may be less suitable

Salary sacrifice lowers your contractual salary, and that can have knock-on effects. A reduced salary figure may affect how much a lender will offer on a mortgage, and it can lower some salary-linked benefits, such as certain statutory payments or life cover set as a multiple of salary. You also cannot sacrifice below the National Minimum Wage. And because the money goes into a pension, you cannot reach it until at least your late fifties; the minimum pension access age is rising to 57 in 2028. If you might need the money before then, an ISA may suit you better, which is covered in ISA vs pension: which should come first?

What to think about before 2029

There is no need to rush. The current rules run unchanged until April 2029, and even then the first £2,000 a year keeps its full advantage. It helps to know roughly how much you sacrifice each year, so you can see whether you are anywhere near the cap, and to keep an eye on any changes your employer makes to its scheme as the date approaches. For most people the sensible course is to carry on, rather than unwind a useful arrangement years early over a change that may affect only part of it.

Use the calculator

The Salary Sacrifice Calculator estimates your take-home pay reduction, the pension contribution, any employer National Insurance give-back and the value per £1 of net pay sacrificed. It reflects the current rules; from April 2029 the National Insurance saving on amounts above £2,000 a year would be smaller than it shows today.

See how it fits your bigger picture

How much to sacrifice is partly a question about your whole financial position, not just this year’s tax. The Wealth Planner brings your pension together with your savings, investments and property, and projects how that position could grow, so you can see what a given level of pension contribution does for your long-term picture.

Related guides

- Salary sacrifice examples at £40k, £50k, £60k, £80k and £100k

- Is salary sacrifice worth it below £50,270?

- What is the 60% tax trap?

- ISA vs pension: which should come first?

Sources and useful reading

- GOV.UK: salary sacrifice reform for pension contributions from 6 April 2029

- GOV.UK: workplace pension payments and salary sacrifice

- House of Commons Library: National Insurance Contributions (Employer Pensions Contributions) Bill

Common questions

A few questions that come up often on this topic.

Does salary sacrifice reduce tax and National Insurance?

At the moment, yes, in many schemes. Because the sacrificed amount is paid by your employer into the pension rather than as salary, it can avoid both Income Tax and National Insurance. From April 2029, the National Insurance saving is capped at the first £2,000 sacrificed each year.

What is changing in April 2029?

From 6 April 2029, only the first £2,000 you sacrifice into a pension each year will be free of National Insurance. Amounts above £2,000 will have both employee and employer National Insurance applied. Income Tax relief is not affected.

Will salary sacrifice still be worth it after 2029?

For most people, yes. Below £2,000 a year nothing changes. Above it, you keep full Income Tax relief and lose only the National Insurance saving on the excess, so it stays at least as efficient as an ordinary pension contribution.

Does the £2,000 cap include my employer's own contributions?

The cap applies to the amount you sacrifice from your salary. Ordinary employer contributions made outside a salary sacrifice arrangement stay free of National Insurance.

Is salary sacrifice better than normal pension contributions?

It can be, mainly because of the National Insurance saving, which a normal contribution does not give you. After 2029 that edge applies to the first £2,000 a year. The lower salary can also affect borrowing and some benefits, so it is not automatically better.

Should I salary sacrifice below £50,270 or £100,000?

Those are common thresholds to test, because they mark the higher-rate band and the point where the Personal Allowance starts to be withdrawn. The right level still depends on affordability, your pension allowance, when you need the money and your employer's scheme.

Can salary sacrifice affect my mortgage application or statutory pay?

It can. Because it lowers your contractual salary, some lenders may offer less, and some salary-linked payments can be lower. Ask your employer how its scheme reports your salary to lenders and for statutory calculations.

If you want to contribute beyond your workplace scheme

Salary sacrifice runs through your workplace pension. If you want to add more than the scheme allows, or its fund choice is limited, some people open a personal pension, or SIPP, alongside it. The Knowledge Hub covers opening a personal pension and what to look for in a SIPP provider.

This article is for general information only. It is not financial advice, pension advice, tax advice or a personal recommendation. Salary sacrifice affects pay, pension contributions and tax treatment, so the right answer depends on your own situation and employer scheme.

Where pension investing is discussed, remember that investing involves risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns. Tax and pension rules can change.