Should I Overpay My Mortgage or Invest?

Reviewed 7 June 2026. A decision guide for weighing the guaranteed saving from overpaying against the uncertain upside of investing; not a recommendation to do either. Figures reflect the 2026/27 UK tax year.

This is one of the most common money questions in the UK, and one of the hardest, because both answers can be right. The useful version of the answer is not “overpay” or “invest”. It is a way of working out which one fits your mortgage rate and your timeframe, and how you feel about taking risk to chase a return.

Overpaying gives you something rare in finance: a known result. You pay less interest, and you often clear the mortgage sooner. Investing keeps more long-term upside in play, but it brings uncertainty and the risk of poor timing over shorter periods. The whole decision turns on how you value certainty against growth that is expected but never promised. This guide works through the maths, shows it with an example, and then covers the parts the maths quietly leaves out.

The clean comparison

Start with the part that is simple to state. A mortgage overpayment works like a guaranteed return equal to your mortgage rate, with no tax due on it and no market risk. If your rate is 5%, every pound you overpay saves you 5% interest on that pound, for certain, for as long as that money would otherwise have sat on the loan. To come out ahead by investing instead, your investment has to earn more than 5% after tax and after charges, and earn it reliably enough to be worth the risk you take to chase it.

That last point is the one people skip past. Beating a 5% guaranteed saving is not the same as expecting a 5% return. A guaranteed 5% and a hoped-for 5% are very different things, because the investment might deliver 9% over a decade or it might fall 20% in a year you happened to need the money. The mortgage saving has no such range; it is the same whether markets soar or slump. So the real question is not only “can I beat my rate?” but “am I willing to take risk to try, and will I hold my nerve when it wobbles?”

A worked example

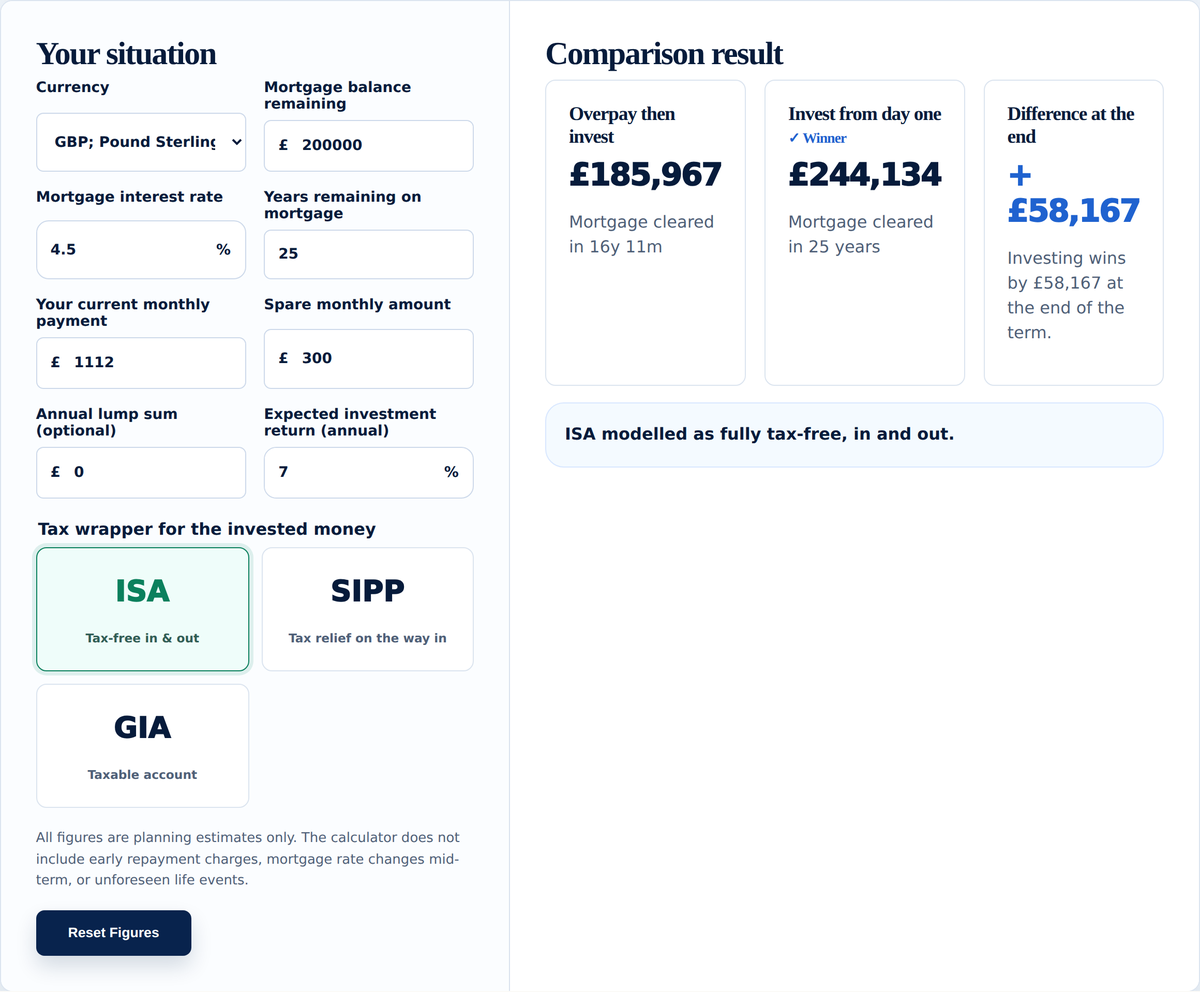

Numbers make this concrete. Suppose you have £200 a month spare, and a £180,000 repayment mortgage at 5% with 20 years left to run. You are deciding whether to put that £200 toward the mortgage or into investments each month.

Put it toward the mortgage and the effect is certain. Overpaying by £200 a month on those terms clears the loan several years early and saves many thousands of pounds in interest, because every overpayment stops that pound being charged 5% for the rest of the term. The exact figures depend on your balance and rate, which is what the calculator is for, but the saving is locked in the moment you make the payment.

Put the same £200 into investments and the result is a range rather than a single number. Over 20 years at a steady 7% it would grow into a noticeably larger pot than the interest you would have saved, which is the case for investing. At 3% it would fall short of the guaranteed saving, which is the case against. Those steady percentages are a convenient fiction, though: real returns arrive unevenly, so the same average can leave you well ahead or, after a poor stretch late in the period, behind. The investing case rests on a long horizon and the discipline to stay invested through the bad runs, not on a smooth line.

Where you invest changes the hurdle

The wrapper you would use matters as much as the headline return, because tax decides how much of that return you actually keep.

Inside a stocks and shares ISA, growth and income are sheltered, so the return you compare against your mortgage rate is the full return. You can pay in up to £20,000 across your ISAs in the 2026/27 tax year. If you have ISA allowance going spare, investing looks relatively stronger, because nothing is skimmed off in tax before it competes with the overpayment. One change to keep in mind for later: from April 2027 the amount under-65s can put specifically into a cash ISA drops to £12,000, while the overall £20,000 limit and the stocks and shares allowance stay the same.

In a general investment account, outside any wrapper, gains and dividends can be taxed, which lowers what you keep and raises the bar your investments must clear to beat overpaying. The capital gains exemption is now just £3,000 and the dividend allowance is £500, both small, and dividend tax rates rose in April 2026. A taxable account therefore makes overpaying look relatively better, because the mortgage saving is tax-free while the investment return may not be.

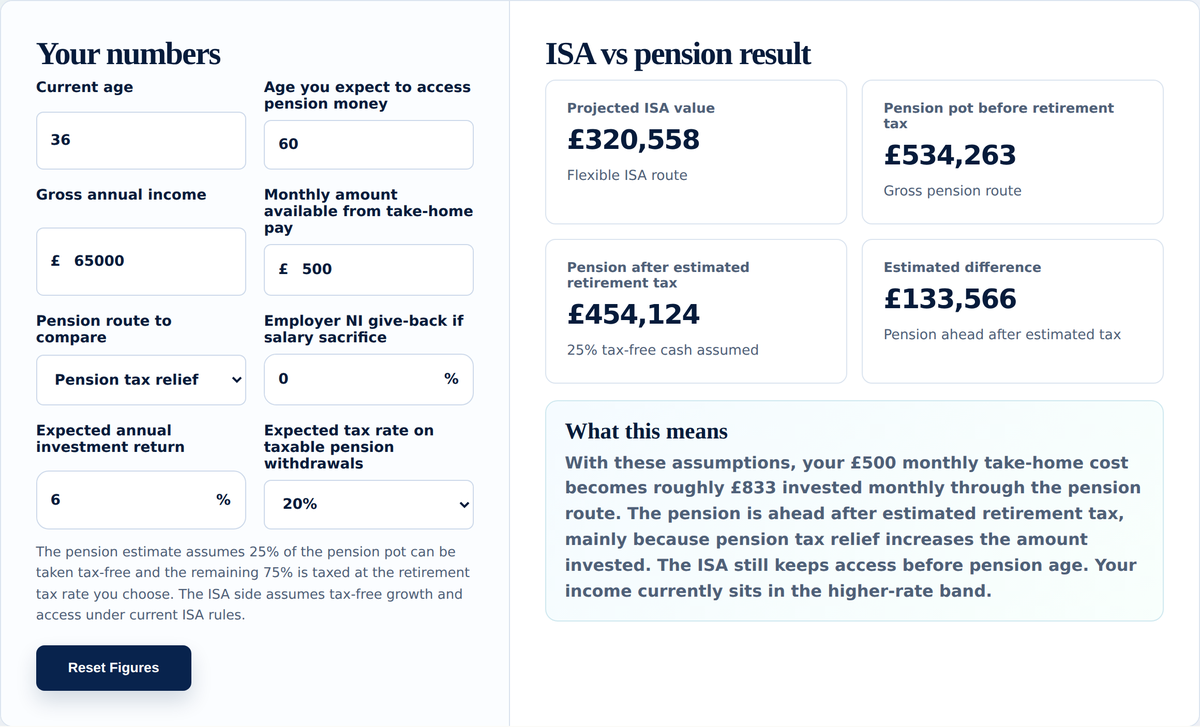

Inside a pension, the comparison can tilt firmly toward investing, and this is the case people most often miss. Pension contributions attract tax relief at your marginal rate. For a higher-rate taxpayer it can take around £60 of take-home pay to put £100 into the pension; for a basic-rate taxpayer, around £80. That uplift is a head start no mortgage overpayment can match. The catch is access, because pension money is locked away until at least age 55, rising to 57 in 2028, so this only helps if you will not need the money before then. With an employer match on top the case is stronger again, which is why the match usually comes first. The ISA vs Pension Calculator and the guide on which should come first work through this in detail, and if salary sacrifice is available to you, the Salary Sacrifice Calculator shows how much the relief is worth.

What about leaving it in savings?

There is a third option people forget, and at today’s rates it earns its place in the decision. If an easy-access savings account pays close to, or more than, your mortgage rate after tax, then holding the cash can beat overpaying while keeping the money within reach. Overpaying saves you your mortgage rate; a savings account paying a similar rate gives you almost the same benefit without sealing the money into the walls of your house.

Two things decide whether this works. The first is tax: savings interest counts toward your Personal Savings Allowance, which shelters £1,000 of interest for a basic-rate taxpayer and £500 for a higher-rate taxpayer, after which interest is taxed and the net rate falls. Holding the savings inside a cash ISA avoids that. The second is the rate itself, since easy-access rates move quickly, so an advantage today can fade at the next change. Cash held with an authorised bank is protected by the FSCS up to £120,000 per person per banking group, a limit raised from £85,000 in December 2025.

An offset mortgage formalises this idea. Your savings sit alongside the mortgage and reduce the interest charged, while remaining accessible, so it behaves like overpaying that you can undo. The trade-off is usually a slightly higher mortgage rate, which is why it tends to suit people who want to keep a large, flexible cash buffer. You can test the cash route in the Savings Calculator.

Why mortgage rates changed this debate

For years this question had an easy answer. When fixed rates sat near 2%, almost any sensible long-term investment was expected to clear that low hurdle comfortably, so investing usually won on the numbers and the main argument for overpaying was peace of mind. Rates look very different now. In mid-2026 the Bank of England base rate is 3.75%, the lowest fixed deals are around 4.3% to 4.5% for borrowers with plenty of equity, typical deals sit somewhat higher, and standard variable rates are near 7% to 8%. A mortgage charging 4.5% or 5% sets a tough, risk-free target, and for some people the guaranteed saving now rivals what they would realistically expect to earn from the market after tax and costs. That is why the question keeps coming back, and why the right answer moves with your rate instead of staying fixed. A rule of thumb from the cheap-money years can give you the wrong answer today.

A couple of things to do first

Before you weigh overpaying against investing, some earlier steps usually come first, because skipping them can turn either choice into a mistake.

Make sure you have an emergency fund, so that neither option leaves you exposed to a surprise bill or a drop in income; the Emergency Fund Calculator and the emergency fund guide help you size one. Clear any expensive debt, such as a credit card balance, since that interest rate is almost always far higher than a mortgage rate, so paying it down beats both options easily. Check whether your employer matches pension contributions, because matched money is an immediate uplift that normally beats overpaying and ordinary investing alike. Only once those are handled does the overpay-or-invest choice become the close call worth modelling. The Knowledge Hub sets out this order in full, and how much should I invest each month covers the investing side.

When overpaying often looks stronger

- Your mortgage rate is high, so the guaranteed saving is large.

- You value certainty and dislike carrying debt.

- Your remaining term is short, leaving less time for investments to recover from a bad spell.

- You would be investing in a taxable account rather than an ISA or pension.

- You already hold plenty of long-term investments elsewhere.

When investing often looks stronger

- Your mortgage rate is low, so the hurdle is easy to clear.

- You have a long timeframe, which gives markets room to ride out volatility.

- You can use an ISA or pension, so growth is sheltered from tax.

- You can access pension tax relief and are happy to lock the money away until pension age.

- You are comfortable with the ups and downs of markets and will leave the money invested.

This is rarely all-or-nothing. Splitting your spare cash, overpaying some and investing the rest, can be both financially reasonable and easier to live with. Many people overpay enough to feel the comfort of a shrinking mortgage, then invest the remainder for long-term growth, keeping a foot in each camp instead of betting everything on one choice.

It is not one decision but several

“Overpay or invest” is really a set of smaller comparisons, and separating them helps. Overpaying versus a pension, covered fully in should I overpay my mortgage or pay into my pension, is often the easiest to call, because pension tax relief gives investing a head start, as long as you can wait until pension age. Overpaying versus a stocks and shares ISA is closer, and turns mainly on your rate and whether you would really leave the money invested for the long run. Overpaying versus cash savings comes down to whether a savings rate, after tax, beats your mortgage rate. For different return assumptions worked through step by step, see mortgage overpayment vs investing at 3, 4, 5 and 6 percent, and for the situations that tip it toward the mortgage, read where overpaying your mortgage actually wins.

What the maths leaves out

The numbers are only part of this decision, and an honest answer respects what they cannot capture.

Peace of mind is real. A smaller mortgage, or none, helps some people sleep in a way no spreadsheet measures. If certainty matters to you, that is a fair reason to lean toward overpaying even when investing might edge it on paper.

Overpayments are hard to reverse. Once money is in the house, getting it back usually means remortgaging or selling. Some lenders let you borrow overpayments back, but many do not. Money invested in an ISA can be reached if life changes, and that access has value.

Behaviour decides the outcome. Investing only wins if you actually invest the money and then leave it alone. If the spare cash would quietly drift into spending, an overpayment that happens automatically may serve you better than an investment plan you do not keep up.

Your rate may not last. If you are on a fix, your rate will change at some point. The maths that favours one choice today can shift at your next remortgage, so this is worth revisiting rather than treating as settled for good.

Check your overpayment limits first

Most fixed-rate deals let you overpay up to a set amount each year, often around 10% of the balance, before an early repayment charge applies. That charge can be large enough to wipe out the saving you were chasing, so check your own lender’s rules before making a big overpayment. It is also worth asking how your lender applies overpayments: some reduce the term and keep your monthly payment the same, which saves the most interest, while others lower the monthly payment and leave the term unchanged, which eases monthly pressure instead.

A few questions to ask yourself

- What is my mortgage rate, and how does it compare with what I could realistically earn after tax and charges?

- How long is left on the mortgage, and how long until I might need this money?

- Would I be investing inside an ISA or pension, or in a taxable account?

- If I chose to invest, would I really invest the money each month and leave it alone?

- How much does the certainty of a smaller mortgage matter to me, separate from the maths?

Your answers usually point more clearly one way than any single rule could.

Test it with your own numbers

The Mortgage vs Invest Calculator lets you enter your actual mortgage rate, spare monthly amount, tax wrapper and an investment return to test, then shows how the two paths compare over your timeframe. It is built to answer this exact question with your figures rather than a general rule, which is the only way to get an answer that fits your situation.

See how it fits your bigger picture

Overpaying or investing is one piece of a wider position that also includes your pension and your other goals. The Net Worth Calculator shows where you stand today, and the Wealth Planner brings everything together into a single view and projects how your overall wealth could change, which helps you judge whether reducing debt or building investments does more for where you are heading.

Related guides

- Where overpaying your mortgage actually wins

- Mortgage overpayment vs investing at 3, 4, 5 and 6 percent

- How much emergency fund do I need?

- ISA vs pension: which should come first?

- How much should I invest each month?

Sources and useful reading

- GOV.UK: Individual Savings Accounts

- GOV.UK: Capital Gains Tax rates and allowances

- GOV.UK: tax on savings interest and the Personal Savings Allowance

- Your Wealth Calculator: methodology and assumptions

Common questions

Questions people often have before they decide.

Is it better to pay off my mortgage or invest?

It depends on your mortgage rate, where you would invest, your timeframe and how you feel about risk. A higher mortgage rate raises the guaranteed saving from overpaying and makes it harder for investing to beat.

What return do I need to beat my mortgage by investing?

Roughly your mortgage rate, but after tax and charges, and with enough margin to justify the risk. A 5% mortgage means your investments need to clear about 5% after costs to win on the numbers, and there is no guarantee they will in any given year.

Should I overpay my mortgage before investing?

Usually not before you have an emergency fund, and not before taking any employer pension match, which is normally the best return of all. After those, the choice between overpaying and investing is personal.

Is overpaying my mortgage risk-free?

The interest saving itself is certain, but it is not cost-free. The money becomes hard to access again, and you give up the chance of higher investment growth. Certain is not the same as without any downside.

Should I overpay my mortgage or pay into my pension?

Pension contributions attract tax relief at your marginal rate, which gives investing a head start that overpaying cannot match, so on the numbers the pension often wins. The trade-off is access, since pension money is locked until at least age 55, rising to 57 in 2028. If you can wait that long, the pension is usually stronger, especially with an employer match.

Should I overpay my mortgage or put the money in savings?

If a savings account pays close to or more than your mortgage rate after tax, holding accessible cash can match most of the benefit of overpaying while keeping the money within reach. Watch the tax on interest above your Personal Savings Allowance, and remember savings rates can change quickly.

Does overpaying reduce my monthly payment or my term?

That depends on your lender and the option you pick. Some lenders shorten the term and keep the payment the same, which saves the most interest, while others lower the monthly payment and keep the term.

Should I still overpay if I have a low fixed rate?

A low rate is an easy hurdle for investing to clear, so the numbers often favour investing. Even so, the certainty of a smaller mortgage has real value to some people, so it is not only about the maths.

Can I get overpayments back if I need the money later?

Often not easily. Some lenders let you borrow back overpayments, but many do not, so money paid into the mortgage is usually harder to reach than money held in an ISA.

How much can I overpay without a penalty?

Most fixed deals allow overpayments of around 10% of the balance each year before an early repayment charge applies, but the exact limit varies by lender and deal. Check your own terms before making a large overpayment, because the charge can cancel out the interest saving.

Does overpaying my mortgage affect my credit score?

Overpaying does not harm your credit score, and reducing what you owe is generally seen positively. Fully repaying and closing the mortgage simply removes that account, which has little lasting effect. Overpaying is a financial decision rather than a credit-building one.

If you decide to invest

If you weigh it up and decide to invest rather than overpay, you will need somewhere to do it, usually a stocks and shares ISA opened through an investment platform. The Knowledge Hub explains how to start investing and what to look for in an ISA platform.

This article is for general information only. It is not financial advice, mortgage advice, investment advice or a personal recommendation. The examples are here to help you compare the trade-offs, but they cannot tell you whether overpaying, investing or doing both is right for your circumstances.

Mortgage overpayments may reduce flexibility, and investments involve risk. The value of investments and any income from them can go down as well as up. You may get back less than you put in, and past performance is not a guide to future returns. Tax rules and allowances depend on your circumstances and may change.